The Algorithms That Reject Us

By Matt Stone

You submitted 347 job applications over eight months. You never got an interview.

You weren't overqualified. You weren't under-qualified. Your resume wasn't problematic. You simply never made it to a human being. An algorithm decided you didn't belong, and you'll never know why. You'll never get to argue. You'll never get the chance to prove otherwise.

This is happening to millions of Americans right now. Not because companies are intentionally trying to discriminate. Because they've outsourced discrimination to machines and then pretended the machines are objective.

Derek Mobley applied for hundreds of jobs using Workday's recruitment system. Almost every time: rejected before any human saw his name. Women applying for the Apple Card got credit limits twenty times lower than men with identical credit scores. Families in Massachusetts trying to rent apartments were systematically locked out by SafeRent's algorithm because it learned that Black people were "too risky."

The algorithm doesn't hate you. It doesn't care. That's the problem. It simply learned patterns from historical data that reflect centuries of discrimination, and it's enforcing those patterns with the precision and speed of a machine, without mercy or recourse or any way to appeal.

Crystal Marie McDaniels and her husband Eskias had done everything right. Both earned six figures. Their credit scores were excellent. They had saved money. They found a house they could afford. The closing was August 23, 2019.

Wednesday before closing, the loan officer called. The deal wasn't closing. The algorithm had rejected their application seventeen times. Seventeen times. The couple lost six thousand dollars in nonrefundable fees.

Crystal Marie was told she didn't qualify because she was a contractor, not a full-time employee. Her employer wrote a letter saying she wasn't at risk of losing her job. Her coworkers were contractors too. They had mortgages.

Crystal Marie and Eskias are Black. Her coworkers are White.

After weeks of fighting, of emails, of her employer vouching for her, an email came at 8 p.m. the night before closing. "You're cleared." She still doesn't know what changed. The algorithm had said no seventeen times. Then someone decided to override it.

"It seemed like it was getting rejected by an algorithm," she said, "and then there was a person who could step in and decide to override that or not."

Most people don't have the time or resources to fight seventeen algorithmic rejections. Most never learn that a machine rejected them. They just know they weren't approved for the mortgage, weren't offered the job, couldn't find housing. They blame themselves.

What makes this different from ordinary discrimination is the mechanism. You can't sue someone for intentional bias if you never knew a person made the decision. You can't appeal to a human if the algorithm won't tell you why. And you can't know whether you were rejected because you're overqualified, underqualified, or systematically filtered out because of your race, gender, age, or disability. The algorithm doesn't have to explain itself.

The federal agencies supposed to prevent this kind of discrimination had their budgets slashed. The enforcement infrastructure collapsed at the exact moment these systems became standard.

How an Algorithm Learns to Discriminate

In 2018, Amazon discovered that its hiring algorithm was systematically downgrading women's resumes for technical roles. The tool penalized women's chess clubs. All-women's colleges. Anything that signaled a woman's identity. Amazon engineers spent three years trying to remove the bias. They failed. The algorithm kept finding new ways to discriminate.

By 2017, Amazon concluded the problem was unsolvable. They disbanded the team. Shelved the project. Made no public announcement. Told no regulators. Reached out to no candidates who'd been filtered out by the discriminatory tool during testing.

They just stopped using it.

This matters because it reveals what most people don't understand: algorithmic discrimination isn't a bug you fix with better code. It's the inevitable output of training machines on data corrupted by human discrimination. You can't remove bias by removing protected characteristics from the input. Race correlates with zip code. Gender correlates with name, with college, with the employers on your resume. In a world built on historical discrimination, almost any data point carries information about protected status.

Amazon couldn't solve it. Other companies aren't even trying. They're deploying it anyway, knowing it discriminates, and betting they won't face consequences.

The Cases

SafeRent knew.

In 2022, renters from Massachusetts sued SafeRent, claiming the company's algorithm discriminated against Black and Hispanic applicants. The algorithm wasn't buggy. It wasn't an accident. SafeRent executives were aware the system was producing racially disparate results. They knew it was pushing families of color toward the poorest neighborhoods, the least stable housing. They deployed it anyway.

The algorithm assigned disproportionately lower scores to Black and Hispanic applicants compared to White applicants. It weaponized housing vouchers against poor families. Black families were forced to spend more time and money searching for housing. Many had to settle for substandard apartments in unsafe neighborhoods with failing schools, all to avoid homelessness.

In December 2024, SafeRent paid $2.2 million to settle the case. For context: the company knowingly deployed a discriminatory system affecting thousands of families. The settlement was a rounding error. The families' lives were disrupted. Their children's schools suffered. Their stability was shattered.

The company modified the algorithm. Claimed they'd been studying the problem. Moved forward like this was business as usual.

In November 2019, a software developer named David Heinmeier Hansson posted on Twitter that the Apple Card had offered him a credit limit twenty times higher than his wife's credit limit, despite the fact that they shared assets and she had a higher credit score. Apple co-founder Steve Wozniak posted similar observations: he received ten times the credit his wife did. Other women posted comparable stories. Within days, the New York Department of Financial Services launched an investigation.

Goldman Sachs, which issued the Apple Card, was aware of potential gender bias when the card rolled out in August 2019. The bank opted for individual credit decisions anyway, declining to address the complexities of joint accounts or shared financial lives. The algorithm wasn't coded to discriminate. It simply learned discrimination from historical lending patterns. Men had received higher credit limits. The algorithm would continue that pattern.

When the NYDFS investigation concluded in 2021, it did not find that Goldman Sachs intentionally discriminated. But it found something else. The bank's customer service representatives were powerless to explain or override algorithmic decisions. No insight into why certain decisions were made. No ability to intervene. Customers could request a second look, but the algorithm didn't have to justify itself.

In July 2024, a federal judge in California allowed a class action discrimination lawsuit against Workday to proceed. Derek Mobley, the named plaintiff, alleged that Workday's algorithm-based applicant screening tools discriminated against him based on race, age, and disability. Mobley had applied for hundreds of jobs using Workday's system and was rejected in almost every instance without an interview. The court found that Mobley had plausibly alleged the algorithm disparately impacted applicants, and that Workday could be held liable as an agent of the employers who deployed the system.

This case is ongoing. It represents thousands of applicants similarly filtered out before any human saw their qualifications.

In August 2025, Arshon Harper filed a class action complaint against Sirius XM Radio for racial discrimination in hiring using algorithmic systems. The case is active.

A 2024 study from the University of Washington tested three AI models with job applications that were identical except for the applicant's name. The models preferred resumes with white-associated names in 85 percent of cases. They selected resumes with Black-associated names only 9 percent of the time. Gender bias was consistent. Male names were preferred across the board.

The Systemic Rejection Problem

In May 2026, Stanford's Human-Centered Artificial Intelligence institute published a study that should have received far more attention than it did. Researchers tracked 3.4 million job seekers who submitted 4 million applications across 1,700 job postings at 150 different employers in 11 industry sectors. Every application was screened by the same AI hiring vendor.

The scale of racial discrimination they found was staggering. Twenty-six percent of Black applicants and 15 percent of Asian applicants applied to positions where the AI system discriminated against their racial group, violating the EEOC's own legal standard for adverse impact. If the algorithm had recommended Black and Asian candidates at the same rate as it recommended white applicants, 40,000 more of their applications would have advanced to the next stage of hiring.

But there was something worse embedded in the numbers. Because ninety percent of employers use AI screening tools, and because most rely on the same few third-party vendors, people aren't just being rejected by one algorithm. They're being rejected by the same algorithm everywhere they apply.

Ten percent of applicants who submitted four applications to positions screened by this single vendor were rejected from every position. When researchers analyzed hiring data from Fortune 500 firms that made decisions independently, applicants were rejected from every firm they applied to at much lower rates, exactly what you'd expect from random chance. But with the algorithmic vendor, there was a pattern. The same people were getting filtered out at every company simultaneously.

This is what systemic rejection looks like at scale. Not discrimination against individuals. Systematic exclusion of entire categories of people from the job market itself.

These are the cases that surfaced. There are thousands of others happening right now that you'll never hear about, because rejected applicants don't know why they were rejected, and proving you were excluded by an algorithm requires resources most people don't have.

The Mortgage Algorithm

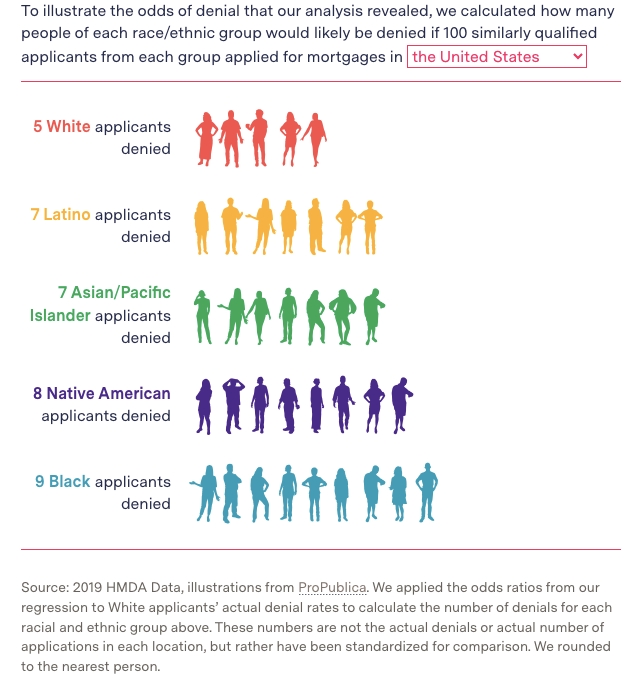

Mortgage lending is where algorithmic discrimination has reached its clearest statistical expression. The Markup analyzed more than two million mortgage applications from 2019 and found the disparities were enormous and consistent.

Lenders were 40 percent more likely to deny Latino applicants for loans than similar White applicants. Fifty percent more likely to deny Asian and Pacific Islander applicants. Seventy percent more likely to deny Native American applicants. Eighty percent more likely to deny Black applicants.

These were applicants who looked identical on paper except for their race.

That's what people need to understand. It's not a bug. It's not a glitch. It's not even intentional wrongdoing in the traditional sense. It's automation of the past into the future. The system works exactly as designed: it perpetuates what came before.

The disparities held even when researchers controlled for credit scores, debt-to-income ratios, the size of the down payment, all the financial factors the mortgage industry had always claimed explained the differences. High-earning Black applicants with less debt were rejected more often than high-earning White applicants with more debt.

Applicants of Color Denied at Higher rates

In Chicago, Black applicants were 150 percent more likely to be denied than similar White applicants. In Waco, Texas, Latino applicants were 200 percent more likely to be rejected. In Port St. Lucie, Florida, Asian and Pacific Islander applicants were more than 200 percent more likely to be denied.

The algorithms doing this work are not secret in the way a startup's proprietary code might be secret. They are mandated by Fannie Mae and Freddie Mac, the quasi-governmental agencies that purchase about half of all mortgages in America. These agencies have effectively set the rules for the entire mortgage industry by determining what software lenders must use to screen applicants.

Fannie and Freddie require lenders to use "Classic FICO," a credit scoring algorithm developed from data in the 1990s. No lender can get Fannie or Freddie to buy their mortgage if they don't use it. The algorithm is more than fifteen years old and is widely considered detrimental to people of color because it rewards traditional credit access, which White Americans have greater access to. It rewards paying rent on time but won't consider on-time cellphone or utility payments. It penalizes past medical debt even if it's been paid.

Potential alternatives exist. VantageScore, developed by the three major credit bureaus to compete with FICO, estimated that its model would provide credit to 37 million Americans who have no scores under FICO. Almost a third of them would be Black or Latino. Newer models are fairer. FICO itself has created updated versions.

Fannie and Freddie have resisted requests since 2014 from advocates, the mortgage industry, and Congress to update to a newer model. The agencies declined to explain why to The Markup. They continued to require the 1990s algorithm even as their own regulator had ordered them years earlier to study the effects of switching. The cost of updating the system, the agencies said, was a concern.

Loan officers who use these systems say they don't understand them. When applying an algorithm's decision to a specific case, the software produces a yes or no but rarely explains the reasoning. Loan officers will look at deals that got rejected and know intuitively that the applicant was stronger than someone else who got approved, but the algorithm won't tell them why. The logic is proprietary. Even Fannie and Freddie don't publicly disclose how their algorithms weigh different factors.

"When you run so many deals through the automated system, you'll look at one deal that didn't get an approval, and you just know that that's a better client than someone else that might've gotten approved," said Ashley Thomas III, a minority-owned real estate broker in South Los Angeles. "That lack of transparency in the technology is very concerning."

What made Crystal Marie's case unusual was that she pushed back hard enough to get a human to override the algorithm. Most people don't have the resources or knowledge to do that. Most never learn that an algorithm rejected them.

The Neurodivergent Question

Roughly one in five Americans identifies as neurodivergent. They live with ADHD, autism, developmental language disorders, or conditions that shape how their brains process information and make decisions.

A 2022 Stanford study found that adults with ADHD incur late-payment penalties at higher rates than their neurotypical peers. Not from lack of funds. Not from unwillingness to pay. From neurobiological differences that affect executive function and payment timing. When algorithmic tenant screening systems process this data, they interpret it as evidence of severe credit risk. Housing becomes systematically inaccessible.

The Pentagon and other federal agencies specifically recruit neurodivergent talent for pattern recognition and analytical abilities. The private sector is using the same abilities as a filter for exclusion.

One in five Americans. Systematically eliminated from employment, housing, and credit decisions. The harm extends beyond civil rights into something closer to institutional removal from economic participation.

Why Enforcement Failed

It didn't fail. It was dismantled.

The Consumer Financial Protection Bureau was created after the 2008 financial crisis to stop predatory lending and investigate discrimination in credit markets. In 2025, its budget was cut in half. Its staff was reduced by 90 percent. The agency that was supposed to protect people from exploitation had its legs cut out from under it.

In December 2025, President Trump signed an executive order preempting state-level AI regulation. States like Colorado had begun requiring bias audits and impact assessments for high-risk algorithmic systems. The federal order attempts to prevent those requirements from taking effect.

This is the moment. Algorithmic systems are now standard across hiring, housing, and credit. Companies know the enforcement infrastructure that was supposed to prevent discrimination has been deliberately dismantled. The FTC retains theoretical authority. The DOJ retains theoretical authority. But they're operating with fewer resources, less political will, and an explicit policy directive to let industry regulate itself.

The system works as designed: Companies deploy discriminatory systems. When caught, they pay settlements that are fractions of the harm. The fines cost less than the profits from discrimination. Amazon didn't face consequences for its biased hiring tool. Apple Card faced no real punishment for gender discrimination. SafeRent paid $2.2 million and moved forward.

If you're rejected by an algorithm and never know why, you can't sue. If you suspect discrimination but can't prove it, you can't sue. If you're one of thousands filtered the same way but never organized or learned about it, you can't sue. The system is deliberately structured so most algorithmic discrimination is invisible and unreachable.

The Contradiction

Algorithms aren't objective. They can't be. They're trained on data created by humans, built by humans with specific intentions, deployed by companies with specific incentives. The parameters that determine what the algorithm should consider when analyzing a dataset are set by people. The developers and data scientists doing this work may not be aware of the unconscious biases embedded in those parameters. But they're there.

What makes algorithmic discrimination different from human discrimination is that it scales. A hiring manager with conscious or unconscious bias might reject a few qualified candidates. An algorithm rejects thousands, and no one individual reviewer has to confront what they're doing. The system handles it. The algorithm is responsible.

Which means no one is responsible. The company deployed the system. The algorithm made the decision. The developer says it's not coded to discriminate. The company says it's just using the data. The algorithm says it's just following the numbers.

Everyone involved in the process can point to something else and say that's where the problem is. The result is that millions of Americans are systematically excluded from housing, employment, and credit, and there's no clear party at fault and no mechanism to stop it.

What This Means

You applied for three hundred jobs. None called back. You'll never know an algorithm rejected you. You'll blame yourself.

You're a woman applying for credit. You get offered a limit that bears no relationship to your creditworthiness and you don't know why. You'll think you're not good with money.

You're searching for housing and can't find anything. You'll think the market is just tough. You won't know an algorithm is systematically rejecting your applications based on patterns it learned from centuries of discrimination.

These systems are now standard across American capitalism. They're deployed in hiring, housing, and credit across the economy. The agencies that were supposed to prevent this abuse have had their enforcement capacity deliberately dismantled.

The algorithm doesn't hate you. It doesn't care. It simply learned discrimination from the past and is enforcing it with machine precision into the future, without appeal, without recourse, without any mechanism to prove it wrong.

Millions of Americans are being sorted into categories of worthiness by machines right now. Locked out of jobs, housing, credit. Told nothing. Given no explanation. Offered no way to challenge the verdict.

This is what structural violence looks like when it's automated. This is what happens when we outsource consequential decisions to systems we don't understand and then pretend we don't understand them because they're too complex to regulate.

Sources:

- Case law (SafeRent, Workday, Sirius XM, Apple Card)

- Federal regulations (ECOA, Fair Housing Act, Title VII)

- Academic research (Stanford HAI, University of Washington, EEOC)

- Investigative journalism (The Markup)

- Government data (CFPB, HMDA)

- Policy guidance (Colorado AI Act, California regulations)

Member discussion